Fantastic Governmental Fund Balance Sheet Common Size Statement Of Profit And Loss

Governmental Funds Financial Statements Office Of The Washington State Auditor

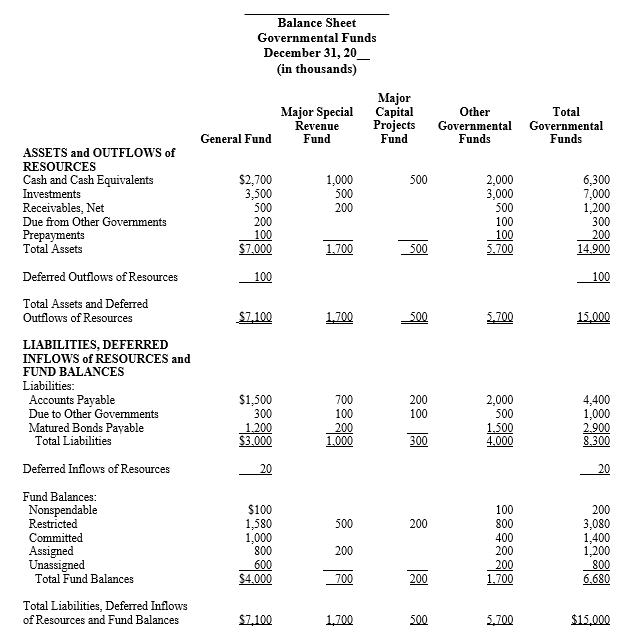

It is essential that differences between GAAP fund balance and budgetary fund balance be fully appreciated. 1 While in both cases fund balance is intended to serve as a measure of the financial resources available in a governmental fund. Fund balance measures how much a government has available to appropriate into the future budgets. These labels are governed by rules adopted by the Governmental Accounting Standards Board GASB. Current Assets Current Liabilities Fund Balance. See Figure 1 Given the basis of accounting these assets are generally current in naturecash short-term investments and short. It summarizes the allocation of all governmental funds and makes it easier to understand how resources are used by the government. The balance sheet of a non-profit organization is prepared in the same manner as in the case of a business enterprise. The governmental funds typically account for tax-supported activities of a government and. Current assets liabilities and fund balances of governmental funds should be displayed in a balance sheet using the following formula.

Fund balance and net assets are the difference between fund assets and liabilities reflected on the balance sheet or statement of net assets.

Within fund balance shown at the bottom of the balance sheet there are several categories. General capital assets and general long-term liabilities are not reported in the governmental fund balance sheet. The assets of the organization are recorded on the Right side and liabilities on the Left side. Current assets liabilities and fund balances of governmental funds should be displayed in a balance sheet using the following formula. Cash from a bond issuance that must be spent within the school system according to the bond indenture98000. In other words with a few exceptions the governmental funds balance sheet reports cash and other financial resources such as receivables as assets and amounts owed that are expected to be paid off within a short period of time as liabilities.

In other words with a few exceptions the governmental funds balance sheet reports cash and other financial resources such as receivables as assets and amounts owed that are expected to be paid off within a short period of time as liabilities. It summarizes the allocation of all governmental funds and makes it easier to understand how resources are used by the government. Cash from a bond issuance that must be spent within the school system according to the bond indenture98000. The balance sheet of a non-profit organization is prepared in the same manner as in the case of a business enterprise. See Figure 1 Given the basis of accounting these assets are generally current in naturecash short-term investments and short. Budget professionals commonly use this same term to describe the net position of governmental funds calculated on a governments budgetary basis. Statement of revenues expenditures and changes in fund balances. Fund balance and net position are the difference between fund assets plus deferred outflows of resources and liabilities plus deferred inflows of resources reflected on the balance sheet or statement of net position. RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THE STATEMENT OF NET POSITION June 30 2018 Exhibit B-1a Dollars in Thousands Total fund balances - governmental funds see Exhibit B-1 8757567 Amounts reported for governmental activities in the Statement of Net Position are different because. General capital assets and general long-term liabilities are not reported in the governmental fund balance sheet.

The financial statements used to present governmental funds are. When budgets are established they are compiled at the fund level. The unrestricted fund balance is the portion of that total fund balance that is not restricted in any way and can be spent however the government chooses to. In the governmental funds balance sheet there are no lines specific to lease accounting as the short - term lease is treated as an expenditure for rent while the long - term non - ownership - transferring lease is treated as both an expenditure and an other financing source. The following are some of the assets reported by this government. These labels are governed by rules adopted by the Governmental Accounting Standards Board GASB. Fund balance and net assets are the difference between fund assets and liabilities reflected on the balance sheet or statement of net assets. Within fund balance shown at the bottom of the balance sheet there are several categories. Current assets liabilities and fund balances of governmental funds should be displayed in a balance sheet using the following formula. The balance sheet of a non-profit organization is prepared in the same manner as in the case of a business enterprise.

It is essential that differences between GAAP fund balance and budgetary fund balance be fully appreciated. The balance sheet of a non-profit organization is prepared in the same manner as in the case of a business enterprise. Fund balance and net assets are the difference between fund assets and liabilities reflected on the balance sheet or statement of net assets. The governmental funds typically account for tax-supported activities of a government and. Within governmental funds equity is reported as fund balance. It summarizes the allocation of all governmental funds and makes it easier to understand how resources are used by the government. Statement of net position. See Figure 1 Given the basis of accounting these assets are generally current in naturecash short-term investments and short. A Total fund balance in the general fund in excess of nonspendable restricted committed and assigned fund balance ie surplus. Budget professionals commonly use this same term to describe the net position of governmental funds calculated on a governments budgetary basis.

The following are some of the assets reported by this government. These labels are governed by rules adopted by the Governmental Accounting Standards Board GASB. Budget professionals commonly use this same term to describe the net position of governmental funds calculated on a governments budgetary basis. In other words with a few exceptions the governmental funds balance sheet reports cash and other financial resources such as receivables as assets and amounts owed that are expected to be paid off within a short period of time as liabilities. Current assets liabilities and fund balances of governmental funds should be displayed in a balance sheet using the following formula. Cash from a bond issuance that must be spent within the school system according to the bond indenture98000. Statement of net position. General capital assets and general long-term liabilities are not reported in the governmental fund balance sheet. Within governmental funds equity is reported as fund balance. The unrestricted fund balance is the portion of that total fund balance that is not restricted in any way and can be spent however the government chooses to.

See Figure 1 Given the basis of accounting these assets are generally current in naturecash short-term investments and short. Statement of fund balance is a part of the balance sheet that governmental entities are required to prepare every year. Proprietary and fiduciary fund equity is reported as net position. These labels are governed by rules adopted by the Governmental Accounting Standards Board GASB. Statement of revenues expenditures and changes in fund balances. Instead General Fund or Accumulated Fund appears on the Balance Sheet. The unrestricted fund balance is the portion of that total fund balance that is not restricted in any way and can be spent however the government chooses to. Statement of net position. In other words with a few exceptions the governmental funds balance sheet reports cash and other financial resources such as receivables as assets and amounts owed that are expected to be paid off within a short period of time as liabilities. Fund balance and net assets are the difference between fund assets and liabilities reflected on the balance sheet or statement of net assets.