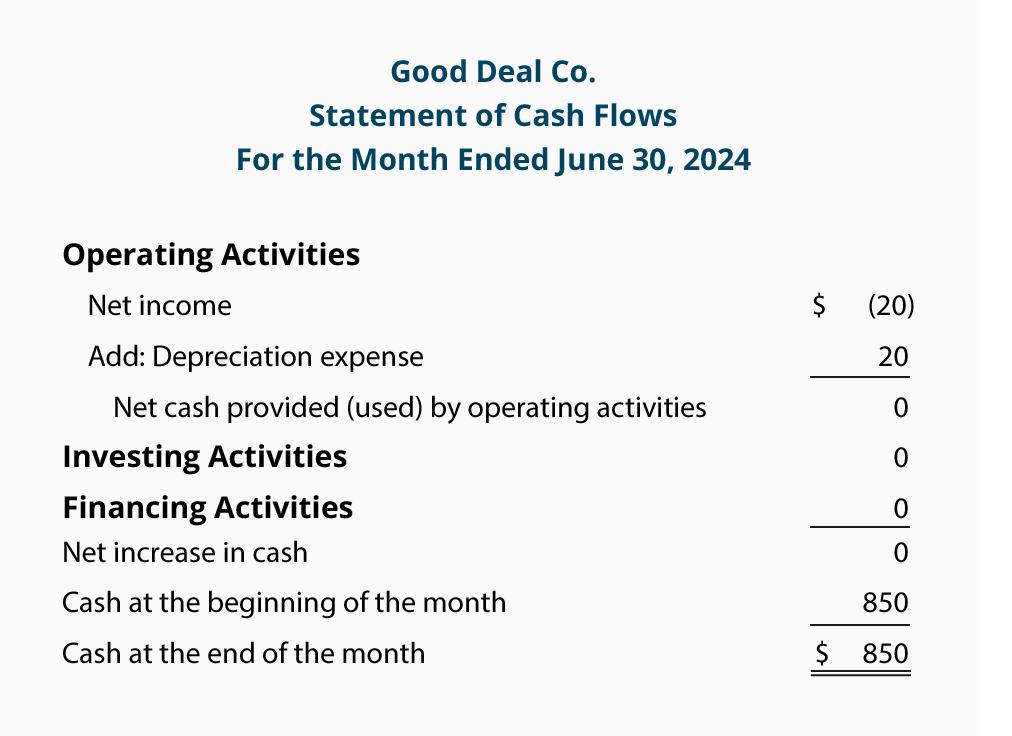

The provision for credit losses is treated as an expense on the. The sources of information appearing in the table can be used to prepare a cash flow statement. The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet collected from the debtors. Uncollectible Accounts and the Cash Flow Statement. The provision is used under accrual basis accounting so that an expense is recognized for probable bad debts as soon as invoices are. What is the treatment for bad debts written off against provision for bad debts in cash flow statement. Thus Bad Debts now has a zero balance and Provision for Bad Debts has a lower balance than before. Browse more Topics under Financial Statements An Introduction to Financial Statements. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. It may be included in the companys selling.

Only change increase or decrease in provision for doubtful is shown in the income statement.

While accounts receivable is an asset provision for bad and doubtful debts is a contra asset meaning that provision is to be deducted from accounts receivable on the balance sheet. Provision for bad debts is the estimated percentage of total doubtful debt that needs to be written off during the next year. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. It is identical to the allowance for doubtful accounts. It depends what the provision is. When increase then expense deducted from profit and when decrease then income added in profits.

The provision for credit losses PCL is an estimation of potential losses that a company might experience due to credit risk. Uncollectible accounts being written off as bad debt expense have no impact on cash flow statements except in the most indirect manner. Uncollectible Accounts and the Cash Flow Statement. When increase then expense deducted from profit and when decrease then income added in profits. That gives you a more realistic picture of your businesss income than assuming every receivable will be paid in full. For calculating cash flow from operating activitiesprovision for doubtful debts is _____ the profit made during the year added todeducted from. It may be included in the companys selling. Those two provisions are dealt with within the changes in working capital and the TNCA figures respectively. The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet collected from the debtors. While accounts receivable is an asset provision for bad and doubtful debts is a contra asset meaning that provision is to be deducted from accounts receivable on the balance sheet.

While accounts receivable is an asset provision for bad and doubtful debts is a contra asset meaning that provision is to be deducted from accounts receivable on the balance sheet. The provision for credit losses is treated as an expense on the. It may be included in the companys selling. The sources of information appearing in the table can be used to prepare a cash flow statement. For calculating cash flow from operating activitiesprovision for doubtful debts is _____ the profit made during the year added todeducted from. When increase then expense deducted from profit and when decrease then income added in profits. Direct Impact of Bad Debt Under operating activities on the cash flow statement the first line is net income copied over from the income statement. The provision is used under accrual basis accounting so that an expense is recognized for probable bad debts as soon as invoices are. It depends what the provision is. Click here to get an answer to your question Treatment of provision for doubtful debts in cash flow statement aparnamishra501 aparnamishra501 03032019 Accountancy Secondary School answered Treatment of provision for doubtful debts in cash flow statement 1 See answer aparnamishra501 is waiting for your help.

The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet collected from the debtors. Credit Bad Debts by the same amount. The sources of information appearing in the table can be used to prepare a cash flow statement. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. For Quarter 2 due to the receipt of cash from the doubtful debts profit is now higher by 80000 as this effectively reduce  the provision for doubt debts. Provision for Bad Debts Meaning. Cash flows from operating activities. Those two provisions are dealt with within the changes in working capital and the TNCA figures respectively. For calculating cash flow from operating activitiesprovision for doubtful debts is _____ the profit made during the year added todeducted from. Assuming that earlier in Quarter 1 provision for doubtful debts of 100000 is created hence reducing corresponding the profit by the same amount.

Net cash flow or the total resultant change in cash and cash equivalents is calculated using either the direct or indirect method. Cash flows from operating activities. It may be included in the companys selling. The provision for credit losses is treated as an expense on the. Those two provisions are dealt with within the changes in working capital and the TNCA figures respectively. It depends what the provision is. Assuming that earlier in Quarter 1 provision for doubtful debts of 100000 is created hence reducing corresponding the profit by the same amount. That gives you a more realistic picture of your businesss income than assuming every receivable will be paid in full. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. Bad debts are thus included as an expense in the income statement but not included as a line item in the cash flow statement direct method.

The bad debt provision may affect your cash flow statement but it isnt one of the items the cash flow statement records. For Quarter 2 due to the receipt of cash from the doubtful debts profit is now higher by 80000 as this effectively reduce  the provision for doubt debts. Debit the account called Provision for Bad Debts for the appropriate amount. It should be noted that bad debts do however form part of the calculation of cash generated from operations when using the indirect cash flow statement which is the preferred method in the US. It may be included in the companys selling. Browse more Topics under Financial Statements An Introduction to Financial Statements. It depends what the provision is. Those two provisions are dealt with within the changes in working capital and the TNCA figures respectively. 11 November 2017 There is two alternative for this it is advisable that you should do netting of Sundry Debtors closing balance which itself includes provision for Bad doubt ful debts adjustment. Click here to get an answer to your question Treatment of provision for doubtful debts in cash flow statement aparnamishra501 aparnamishra501 03032019 Accountancy Secondary School answered Treatment of provision for doubtful debts in cash flow statement 1 See answer aparnamishra501 is waiting for your help.