Perfect Unsecured Loans Given To Subsidiaries In Cash Flow Statement Balance Sheet Formats

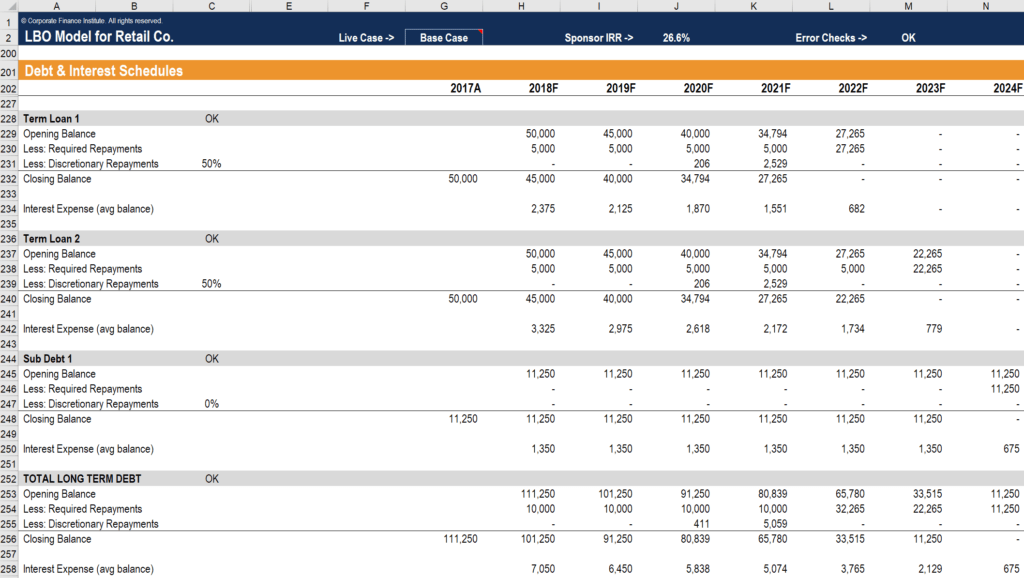

Debt Schedule Timing Of Repayment Interest And Debt Balances

The entity is required prepare the statement of cash flows by classifying such cash flows into operating investing and financing activities. Net Cash Generated Used - Investing Activities 2244 811 CASH FLOW FROM FINANCING ACTIVITIES. In other words a short-term bank loan is a current liability. The worksheet entries produce correct balances for the consolidated statement of cash flows. Prepare the cash flow statement from investing activities of Alpha Creative Ltd for the year ended March31 2019. Where proportionate consolidation is used the cash flow statement should include the venturers share of the cash flows of the investee IAS 737. Proceeds from issue of Equity Shares Including Share Application Money 6. Loan given to subsidiary companies 9618120000 10000000000 Loan repaid by subsidiary companies 6311466000 - Loan given to others 1150000000 - Interest income received 843447292 496312350 Net cash used in investing activities 5551603436 33077591555 C. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of. Because the statement of cash flows is derived from the consolidated balance sheet and income statement the impact of all transfers is already removed.

Classification of cash flows of the entity by activity will enable the users of financial statements to understand the effect of each category of cash flows upon the financial position of the business.

As regards the cash flows of associates joint ventures and subsidiaries where the equity or cost method is used the statement of cash flows should report only cash flows between the investor and the investee. An item on the cash flow statement belongs in the investing activities section if it is the result of any gains or losses from investments in financial markets and operating subsidiaries. As per AS-3 Revised the objective of cash flow statement is to provide information about cash flows of an enterprise which is useful in providing the users of financial statements a basis to assess the ability of an enterprise to generate cash and cash equivalents to utilise those cash flows. A technology loan is tied to a specific technology purchase while a market expansion loan is geared to a specific project that is expected to lead to business growth. Because the statement of cash flows is derived from the consolidated balance sheet and income statement the impact of all transfers is already removed. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of.

Loan in the scope of AASB 9 Financial Instruments. Additions to property plant and equipment in the cash flow statement. The cash flow statement bridges the gap between the income statement and the balance sheet by showing how much cash is generated or spent on operating investing and financing activities for a. As regards the cash flows of associates joint ventures and subsidiaries where the equity or cost method is used the statement of cash flows should report only cash flows between the investor and the investee. Interest on loan received from subsidiary companies 72500. A Cash flow statement discloses net increase or decrease in cash during an accounting period. Prepare the cash flow statement from investing activities of Alpha Creative Ltd for the year ended March31 2019. To profit or loss. Presentation of a statement of cash flows 10 The statement of cash flows shall report cash flows during the period classified by operating investing and financing activities. That is loans that are issued and secured only by the borrowers creditworthiness and not any specific type of collateral like real estate or a piece of new machinery.

Claim received for loss of plant in fire 45500. The entity is required prepare the statement of cash flows by classifying such cash flows into operating investing and financing activities. A Cash flow statement discloses net increase or decrease in cash during an accounting period. Much of the money business owners borrow to manage their cash flow and meet unexpected business expenses are unsecured business loans. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of. Loan given to subsidiary companies 9618120000 10000000000 Loan repaid by subsidiary companies 6311466000 - Loan given to others 1150000000 - Interest income received 843447292 496312350 Net cash used in investing activities 5551603436 33077591555 C. The worksheet entries produce correct balances for the consolidated statement of cash flows. Prepare the cash flow statement from investing activities of Alpha Creative Ltd for the year ended March31 2019. Its financial statement a separate statement containing the salient features of the financial statement of its subsidiary or subsidiaries in such form as may be prescribed. 11 An entity presents its cash flows from operating investing and financing activities in.

An item on the cash flow statement belongs in the investing activities section if it is the result of any gains or losses from investments in financial markets and operating subsidiaries. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of. To profit or loss. Loans and Deposits given 80 272 Receipt of Loans and Deposits given. As per AS-3 Revised the objective of cash flow statement is to provide information about cash flows of an enterprise which is useful in providing the users of financial statements a basis to assess the ability of an enterprise to generate cash and cash equivalents to utilise those cash flows. For intercompany loans receivable with no stated terms the lender also needs to consider the classification and measurement criteria in AASB 9 to determine if the criteria for amortised cost are met. CASH FLOW FROM FINANCING ACTIVITIES. The cash flow statement bridges the gap between the income statement and the balance sheet by showing how much cash is generated or spent on operating investing and financing activities for a. The amounts to be shown under financing or investing cash flows shall be strictly cash paid or received during the period. Reporting Short-Term Bank Loans on the Statement of Cash Flows.

Cash flow loans are similar to other types of unsecured loans such as technology and market expansion loans but they differ from these loans in key ways. Unsecured loans given to subsidiaries 595000. Loans and Deposits given 80 272 Receipt of Loans and Deposits given. Loan given to subsidiary companies 9618120000 10000000000 Loan repaid by subsidiary companies 6311466000 - Loan given to others 1150000000 - Interest income received 843447292 496312350 Net cash used in investing activities 5551603436 33077591555 C. Reporting Short-Term Bank Loans on the Statement of Cash Flows. That is loans that are issued and secured only by the borrowers creditworthiness and not any specific type of collateral like real estate or a piece of new machinery. Therefore no special adjustments are needed to properly present cash flows. A Cash flow statement discloses net increase or decrease in cash during an accounting period. Proceeds from issue of Equity Shares Including Share Application Money 6. The cash flow statement bridges the gap between the income statement and the balance sheet by showing how much cash is generated or spent on operating investing and financing activities for a.

In other words a short-term bank loan is a current liability. Much of the money business owners borrow to manage their cash flow and meet unexpected business expenses are unsecured business loans. Net Cash Generated Used - Investing Activities 2244 811 CASH FLOW FROM FINANCING ACTIVITIES. Classification of certain cash payments and receipts in the statement of cash flows which has led to diversity in practice. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of. To profit or loss. Differences will be reflected in the changes in operating assets and liabilities or as additions to qualifying assets if interest has been capitalised in the cost of these assets. Presentation of a statement of cash flows 10 The statement of cash flows shall report cash flows during the period classified by operating investing and financing activities. That is loans that are issued and secured only by the borrowers creditworthiness and not any specific type of collateral like real estate or a piece of new machinery. Therefore no special adjustments are needed to properly present cash flows.