Out Of This World Comprehensive Income Format Cma Balance Sheet

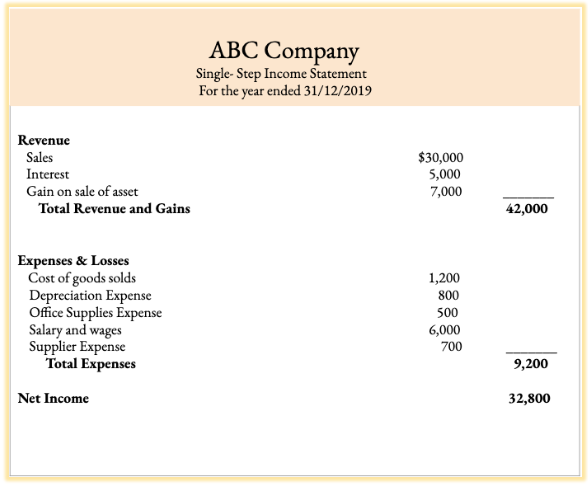

What Is The Single Step Income Statement When To Use It

Unrealized gains or losses on derivatives used in hedging. The net income is the result obtained by preparing an income statement. Knowing these figures allows a company to measure changes in the businesses it has interests in. It usually includes the net income and unrealized income such as unrealized gains or losses on the unoriginal financial instruments. One is operation profit and the second one is non-operation profit. In business accounting other comprehensive income OCI includes revenues expenses gains and losses that have yet to be realized and are excluded from net income on an income statement. The Basics of Comprehensive Income OCI and AOCI The differences between comprehensive income OCI and AOCI are subtle yet critically important. Comprehensive income is the profit or loss in a companys investments during a specific time period. As you can see the statement first lays out the usual line items of the Profit and Loss Statement. Heres What Well Cover.

The items which make up other comprehensive income include.

This is simply translated into the accounting of comprehensive income within the familiar to most report on profit and loss. Unrealized gains or losses on derivatives used in hedging. Comprehensive income includes net income and unrealized income such as unrealized gains or losses on hedgederivative financial instruments and foreign currency transaction gains or losses. The statement of comprehensive income is a financial statement that summarizes both standard net income and other comprehensive income OCI. Colgate SEC Filings As seen from the above statement we have to consider two primary components. Comprehensive income is often listed on the financial statements to include all other revenues expenses gains and losses that affected stockholders equity account during a period.

With the first approach you have just one report called Statement of Income and Comprehensive Income. Comprehensive income includes net income and unrealized income such as unrealized gains or losses on hedgederivative financial instruments and foreign currency transaction gains or losses. 3If a company prepares a statement of comprehensive income then disclosure is required for 1 other comprehensive income classified by nature 2 comprehensive income of associates and joint ventures and 3 total comprehensive incomeThe statement of comprehensive income is discussed in more detail later in the chapter. Other comprehensive income is made up of unrealized gains or losses from the following. The items which make up other comprehensive income include. Comprehensive income is often listed on the financial statements to include all other revenues expenses gains and losses that affected stockholders equity account during a period. Comprehensive Income Net Income Other Comprehensive Income. Comprehensive income sums up all changes in the shareholders equity for a period except those arising from transactions with owners. Comprehensive Income Net Income Other Comprehensive Income OCI. Comprehensive income is made up of a companys overall sales revenue net income and figures for other comprehensive income which are combined to form comprehensive income.

It usually includes the net income and unrealized income such as unrealized gains or losses on the unoriginal financial instruments. Comprehensive income includes net income and unrealized income such as unrealized gains or losses on hedgederivative financial instruments and foreign currency transaction gains or losses. Comprehensive Income Net Income Other Comprehensive Income OCI. Comprehensive income is the profit or loss in a companys investments during a specific time period. Format for Statement of Comprehensive Income Comprehensive income connotes the detailed income statement where we will also include income from other sources along with the income from the main function of the business. This is simply translated into the accounting of comprehensive income within the familiar to most report on profit and loss. It is a broader measure of return earned during period and can be defined as follows. The term comprehensive income consists of 1 a corporations net income which is detailed on the corporations income statement and 2 a few additional items which make up what is known as other comprehensive income. In business accounting other comprehensive income OCI includes revenues expenses gains and losses that have yet to be realized and are excluded from net income on an income statement. This format divided the statement into two different types.

It usually includes the net income and unrealized income such as unrealized gains or losses on the unoriginal financial instruments. Total comprehensive income is therefore equal to net income other comprehensive income 50 million 25 million 75 million. You can think of comprehensive income as an expanded version of net income. The second format of Statement of Comprehensive Income is the multiple-step of the income statement. Comprehensive income includes net income and unrealized income such as unrealized gains or losses on hedgederivative financial instruments and foreign currency transaction gains or losses. One is operation profit and the second one is non-operation profit. Comprehensive income is made up of a companys overall sales revenue net income and figures for other comprehensive income which are combined to form comprehensive income. Net income or net loss the details of which are reported on the corporations income statement plus Other comprehensive income. A variation that occurs in a companys net assets from non-owner sources during a specific period is known as a comprehensive income. With the first approach you have just one report called Statement of Income and Comprehensive Income.

Net income or net loss the details of which are reported on the corporations income statement plus Other comprehensive income. Unrealized gains or losses on derivatives used in hedging. It usually includes the net income and unrealized income such as unrealized gains or losses on the unoriginal financial instruments. This is simply translated into the accounting of comprehensive income within the familiar to most report on profit and loss. Comprehensive Income Net Income Other Comprehensive Income. This format divided the statement into two different types. In its most basic form. These amounts cannot be included on a companys income statement because the investments are still in play. The Basics of Comprehensive Income OCI and AOCI The differences between comprehensive income OCI and AOCI are subtle yet critically important. One is operation profit and the second one is non-operation profit.

It is a broader measure of return earned during period and can be defined as follows. In business accounting other comprehensive income OCI includes revenues expenses gains and losses that have yet to be realized and are excluded from net income on an income statement. Total comprehensive income is therefore equal to net income other comprehensive income 50 million 25 million 75 million. Comprehensive income is the profit or loss in a companys investments during a specific time period. Colgate SEC Filings As seen from the above statement we have to consider two primary components. This is simply translated into the accounting of comprehensive income within the familiar to most report on profit and loss. Net income or net loss the details of which are reported on the corporations income statement plus Other comprehensive income. In its most basic form. The items which make up other comprehensive income include. Comprehensive income for a corporation is the combination of the following amounts which occurred during a specified period of time such as a year quarter month etc.