Supreme Consolidation Accounting Ifrs Company Income And Expense Spreadsheet

Ifrs 10 Summary New Video In The Link Below Youtube

Standards Boards Accounting Standards Codification ASC Topic 810 Consolidations. The IASB International Accounting Standards Board recently issued IFRS 11 Joint Arrangements that eliminates proportionate consolidation as a method to account for joint ventures. The requirement to prepare consolidated financial statements is governed by the Companies Act 2006. Proportional consolidation was a former method of accounting for joint ventures under the International Financial Reporting Standards IFRS that was abolished by. However if it does so it must also adopt the new standards on consolidation IFRS 10 and disclosures IFRS 12 at the same time as well as the revised standards on separate financial statements IAS 27 2011 and equity method accounting IAS 28 2011. 12 Areas where IFRS 10 can affect the scope of consolidation 9 13 IFRS 10 in the context of the overall consolidation package 10 14 Effective date and Transition of IFRS 10 11 2 Scope and consolidation exemptions 12 21 Scope of IFRS 10 13 22 Consolidation exceptions and exemptions 14 3 The control definition and guidance 16. The jointly controlled assets classification in IAS 31 Interests in joint ventures has been merged into joint operations as both types of arrangements generally result in the same accounting outcome. Control Power Exposure or rights to variable returns Ability to use power to affect returns. IFRS 11 classifies joint arrangements as either joint operations or joint ventures. As mentioned at the beginning consolidated financial statements are financial statements of a group in which assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity and with uniform accounting policies IFRS 1019B86-B87.

The requirement to prepare consolidated financial statements is governed by the Companies Act 2006.

GAAP and IFRS related to consolidations are. An entity can elect to early adopt IFRS 11. Standards Boards Accounting Standards Codification ASC Topic 810 Consolidations. A parent entity only prepares consolidated financial statements under the Act if it is a parent at the year end. GAAP and IFRS related to consolidations are. IFRS 10 Consolidated Financial Statements outlines the requirements for the preparation and presentation of consolidated financial statements requiring entities to consolidate entities it controls.

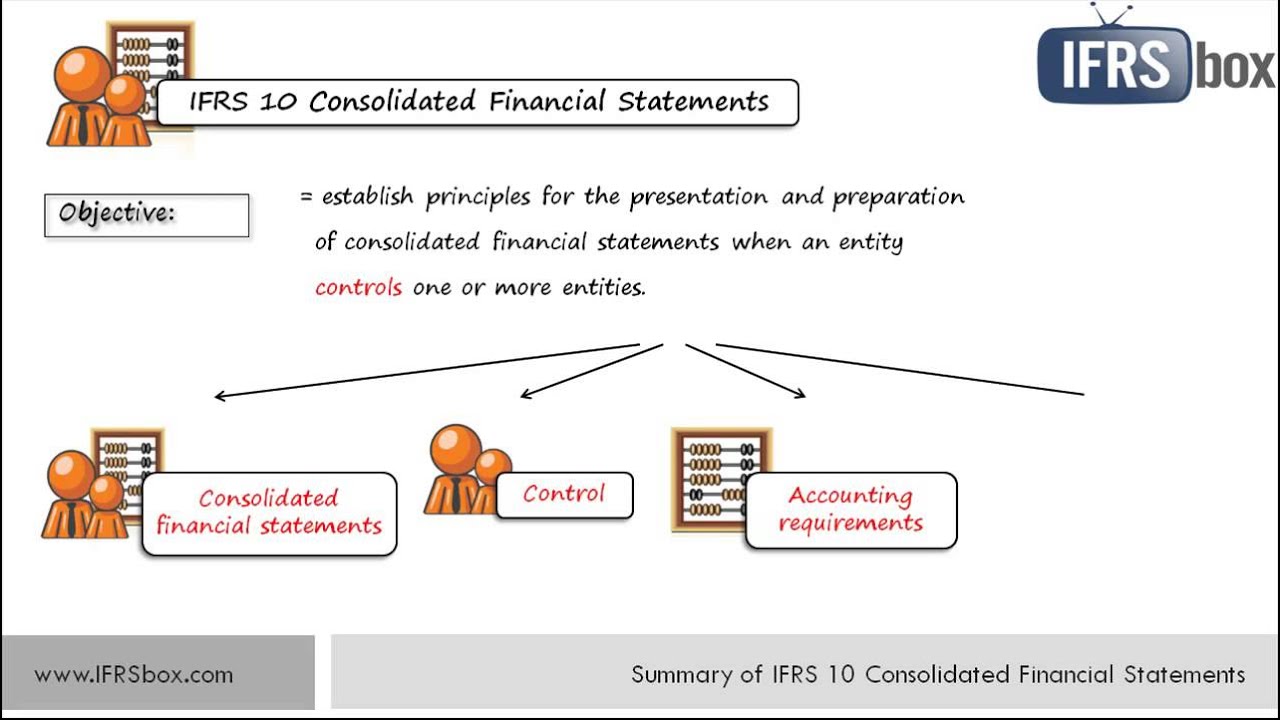

IFRS 11 classifies joint arrangements as either joint operations or joint ventures. However if it does so it must also adopt the new standards on consolidation IFRS 10 and disclosures IFRS 12 at the same time as well as the revised standards on separate financial statements IAS 27 2011 and equity method accounting IAS 28 2011. Requires an entity the parent that controls one or more other entities subsidiaries to present consolidated financial statements. 12 Areas where IFRS 10 can affect the scope of consolidation 9 13 IFRS 10 in the context of the overall consolidation package 10 14 Effective date and Transition of IFRS 10 11 2 Scope and consolidation exemptions 12 21 Scope of IFRS 10 13 22 Consolidation exceptions and exemptions 14 3 The control definition and guidance 16. Standards Boards Accounting Standards Codification ASC Topic 810 Consolidations. Proportional consolidation was a former method of accounting for joint ventures under the International Financial Reporting Standards IFRS that was abolished by. The jointly controlled assets classification in IAS 31 Interests in joint ventures has been merged into joint operations as both types of arrangements generally result in the same accounting outcome. In IFRS the guidance related to consolidations is included in IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities. Significant influence joint control and the appropriate accounting underthe requisite IFRS. IFRS 10 establishes principles for presenting and preparing consolidated financial statements when an entity controls one or more other entities.

The jointly controlled assets classification in IAS 31 Interests in joint ventures has been merged into joint operations as both types of arrangements generally result in the same accounting outcome. IFRS reporters in the UK. In IFRS the guidance related to consolidations is included in IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities. IFRS 10 Consolidated Financial Statements outlines the requirements for the preparation and presentation of consolidated financial statements requiring entities to consolidate entities it controls. The requirement to prepare consolidated financial statements is governed by the Companies Act 2006. Consolidated financial statements IFRS 10 Consolidated Financial Statements establishes principles for the presentations and preparation of consolidated financial statements when an entity controls one or more other entities. As mentioned at the beginning consolidated financial statements are financial statements of a group in which assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity and with uniform accounting policies IFRS 1019B86-B87. The three elements of control which are the basis for consolidation under IFRS 10 are depicted below. Proportional consolidation was a former method of accounting for joint ventures under the International Financial Reporting Standards IFRS that was abolished by. IFRS 11 classifies joint arrangements as either joint operations or joint ventures.

Significant influence joint control and the appropriate accounting underthe requisite IFRS. Standards Boards Accounting Standards Codification ASC Topic 810 Consolidations. As mentioned at the beginning consolidated financial statements are financial statements of a group in which assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity and with uniform accounting policies IFRS 1019B86-B87. He was responsible for advising a multi-national group of over 150 subsidiaries in its adoption of IFRS and the preparation of the groups first IFRS consolidated financial statements. Consolidated financial statements IFRS 10 Consolidated Financial Statements establishes principles for the presentations and preparation of consolidated financial statements when an entity controls one or more other entities. In IFRS the guidance related to consolidations is included in IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities. For years commencing January 1 2013. An entity can elect to early adopt IFRS 11. The three elements of control which are the basis for consolidation under IFRS 10 are depicted below. The jointly controlled assets classification in IAS 31 Interests in joint ventures has been merged into joint operations as both types of arrangements generally result in the same accounting outcome.

Significant influence joint control and the appropriate accounting underthe requisite IFRS. Comparison The significant differences between US. Consolidated financial statements IFRS 10 Consolidated Financial Statements establishes principles for the presentations and preparation of consolidated financial statements when an entity controls one or more other entities. Combine like items of assets liabilities equity income expenses and cash flows of the parent with those of its subsidiaries. As mentioned at the beginning consolidated financial statements are financial statements of a group in which assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity and with uniform accounting policies IFRS 1019B86-B87. Proportional consolidation was a former method of accounting for joint ventures under the International Financial Reporting Standards IFRS that was abolished by. An entity can elect to early adopt IFRS 11. IFRS reporters in the UK. However if it does so it must also adopt the new standards on consolidation IFRS 10 and disclosures IFRS 12 at the same time as well as the revised standards on separate financial statements IAS 27 2011 and equity method accounting IAS 28 2011. The standard was published in May 2011 and is effective from 1 January 2013 1 January 2014 for EU preparers.

I have described the consolidation procedures and their 3-step process in my previous article with the summary of IFRS 10 Consolidated financial statements but let me repeat it here and follow these steps. An entity can elect to early adopt IFRS 11. Control Power Exposure or rights to variable returns Ability to use power to affect returns. The nature of its relationship with the investee eg. The three elements of control which are the basis for consolidation under IFRS 10 are depicted below. Standards Boards Accounting Standards Codification ASC Topic 810 Consolidations. As mentioned at the beginning consolidated financial statements are financial statements of a group in which assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity and with uniform accounting policies IFRS 1019B86-B87. The IASB International Accounting Standards Board recently issued IFRS 11 Joint Arrangements that eliminates proportionate consolidation as a method to account for joint ventures. IFRS 10 Consolidated Financial Statements outlines the requirements for the preparation and presentation of consolidated financial statements requiring entities to consolidate entities it controls. In other words tax.