Beautiful Work State Of Comprehensive Income Statement Financial Activities Charity

Income Statement Definition Explanation And Examples

What is comprehensive income. When the gains and losses crystalize into cash they are usually reflected on the income statement and removed from other comprehensive income. Other comprehensive income OCI is defined as comprising items of income and expense including reclassification adjustments that are not recognised in profit or loss as required or permitted by other International Financial Reporting Standards IFRS. Comprehensive income includes net income and. Total comprehensive income is the combination of profit or loss and other comprehensive. Comprehensive income is the variation in a companys net assets from non-owner sources during a specific period. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement. The statement of comprehensive income is one of the five financial statements required in a complete set of financial statements for distribution outside of a corporation. Notice that we report net income that occurs in the current reporting period in the income statement and also report accumulated net income that hasnt been distributed as dividends in the balance sheet as retained earnings. Other comprehensive income if any.

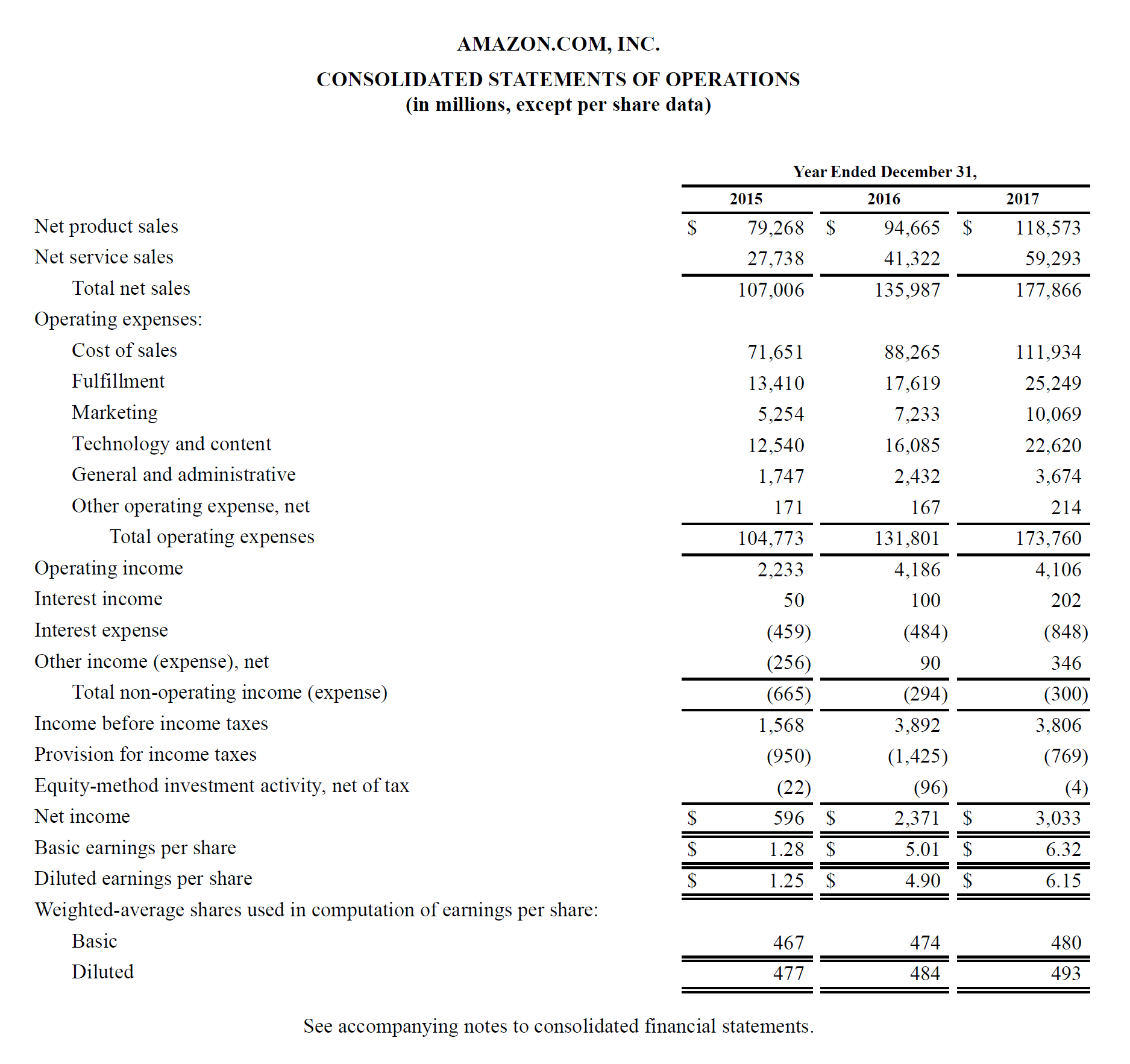

A more complete view of a companys income and revenues is shown by.

In other words it adds additional detail to the balance sheets equity section to show what events changed the stockholders equity beyond the traditional net income listed on the income statement. Comprehensive income is the variation in a companys net assets from non-owner sources during a specific period. In other words it adds additional detail to the balance sheets equity section to show what events changed the stockholders equity beyond the traditional net income listed on the income statement. IAS 1 para 81 allows that all the items of income and expenses recognized in the period. When the gains and losses crystalize into cash they are usually reflected on the income statement and removed from other comprehensive income. The statement of retained earnings includes two key parts.

The main example is the revaluation of tangible assets. State separately in the statement of comprehensive income or in a note thereto amounts earned from a dividends b interest on securities c profits on securities net of losses and d miscellaneous other income. The purpose of the statement of profit or loss and other comprehensive income OCI is to show an entitys financial performance in a way that is useful to a wide range of users so that they may attempt to assess the future net cash inflows of an entity. Statement of Comprehensive Income. Other comprehensive income OCI is defined as comprising items of income and expense including reclassification adjustments that are not recognised in profit or loss as required or permitted by other International Financial Reporting Standards IFRS. Total comprehensive income is the combination of profit or loss and other comprehensive. Comprehensive income for a corporation is the combination of the following amounts which occurred during a specified period of time such as a year quarter month etc. Comprehensive income is the sum of net income and other items that must bypass the income statement because they have not been realized including items like an unrealized holding gain or loss from available for sale securities and foreign currency translation gains or losses. Amounts earned from transactions in securities of related parties shall be disclosed as required under 2104-08 k. The statement of retained earnings includes two key parts.

Other comprehensive income is designed to give the reader of a companys financial statements a more comprehensive view of the financial status of the entity though in practice it is possible that it introduces too much complexity to the income statement. Comprehensive income is the variation in a companys net assets from non-owner sources during a specific period. The gain is not realised until the asset is. Both before-tax and net-of-tax presentations are permitted provided the entity complies withthe requirements in paragraph 220 10-45-12correspond to the - components of other comprehensive income in the statement in which other comprehensive income. Net income or net loss the details of which are reported on the corporations income statement plus. The statement of other comprehensive income represents a companys change in equity during a specific period from transactions and events that are typically non-cash gains and losses. Comprehensive income includes net income and. What is comprehensive income. When the gains and losses crystalize into cash they are usually reflected on the income statement and removed from other comprehensive income. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement.

This is simply an extension of the income statement. When the gains and losses crystalize into cash they are usually reflected on the income statement and removed from other comprehensive income. Comprehensive income is the variation in a companys net assets from non-owner sources during a specific period. In other words it adds additional detail to the balance sheets equity section to show what events changed the stockholders equity beyond the traditional net income listed on the income statement. Statement of Comprehensive Income. Either a si ngle statement of comprehensive income or a statement displaying components of profit or loss separate income statement and a second statement beginning with profit or loss and displaying components of o ther comprehensive income statement of comprehensive income. Other comprehensive income OCI is defined as comprising items of income and expense including reclassification adjustments that are not recognised in profit or loss as required or permitted by other International Financial Reporting Standards IFRS. Amounts earned from transactions in securities of related parties shall be disclosed as required under 2104-08 k. Other comprehensive income if any. A more complete view of a companys income and revenues is shown by.

Comprehensive income is the sum of net income and other items that must bypass the income statement because they have not been realized including items like an unrealized holding gain or loss from available for sale securities and foreign currency translation gains or losses. Comprehensive income is the variation in a companys net assets from non-owner sources during a specific period. Other comprehensive income if any. Income Statement and Statement of Comprehensive are differentiated because IAS 1 gives two options to present the items of incomes and expenses recognized during the period. A more complete view of a companys income and revenues is shown by. The purpose of the statement of profit or loss and other comprehensive income OCI is to show an entitys financial performance in a way that is useful to a wide range of users so that they may attempt to assess the future net cash inflows of an entity. State separately in the statement of comprehensive income or in a note thereto amounts earned from a dividends b interest on securities c profits on securities net of losses and d miscellaneous other income. Total comprehensive income is the combination of profit or loss and other comprehensive. EITHER in a single statement ie. The statement of comprehensive income reports the change in net equity of a business enterprise over a given period.

The main example is the revaluation of tangible assets. The reason for this is that some gains the business makes during the year are not realised gains. The statement of comprehensive income reports the change in net equity of a business enterprise over a given period. A more complete view of a companys income and revenues is shown by. The statement of comprehensive income is one of the five financial statements required in a complete set of financial statements for distribution outside of a corporation. Other comprehensive income OCI is defined as comprising items of income and expense including reclassification adjustments that are not recognised in profit or loss as required or permitted by other International Financial Reporting Standards IFRS. Net income and other comprehensive income which incorporates the items excluded from the income statement. Comprehensive income includes a net income and b other comprehensive income. Comprehensive income includes net income and. What is comprehensive income.