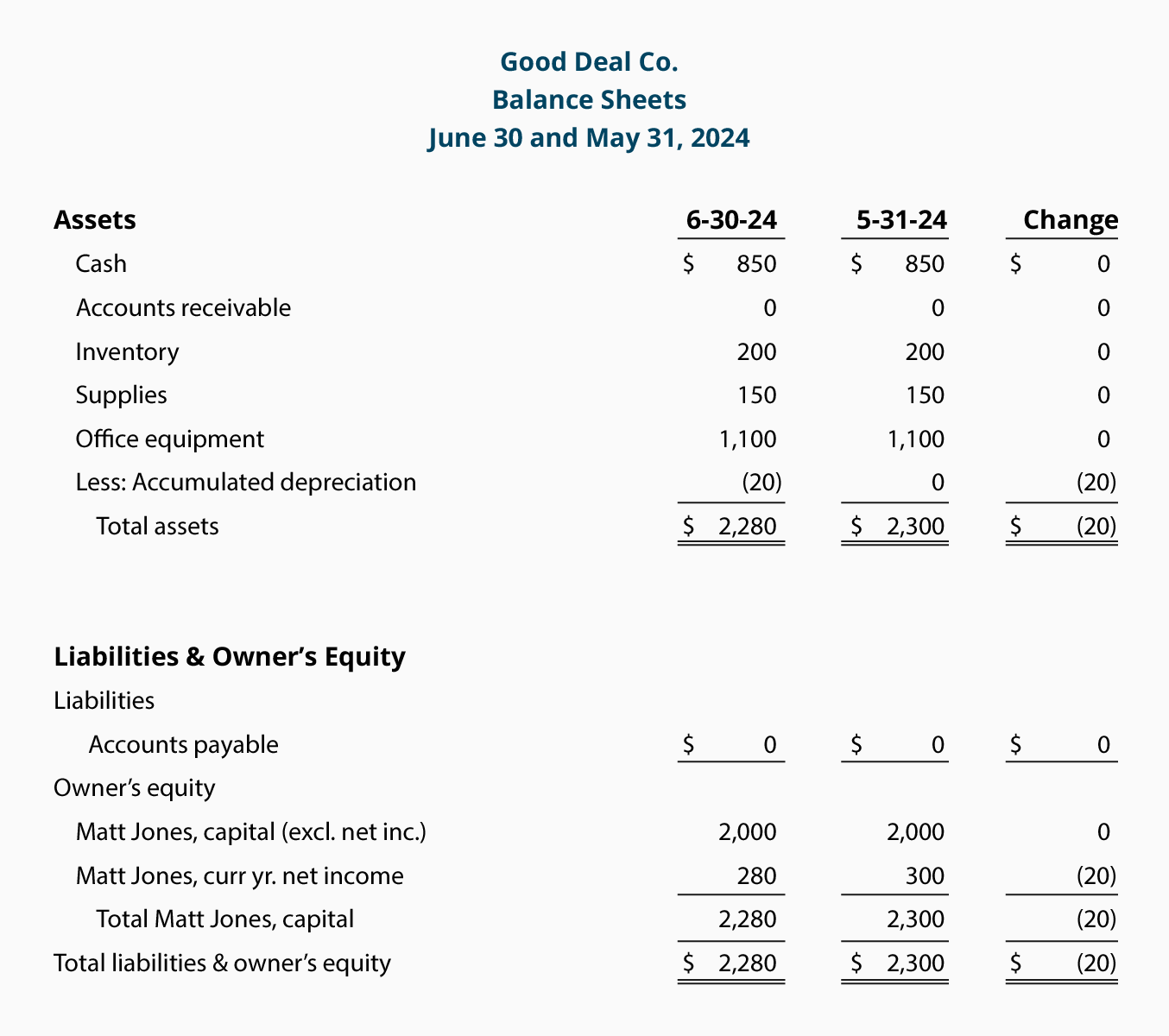

When the asset is sold other otherwise disposed of you should remove the accumulated depreciation at the same time. The accumulated depreciation is shown as a credit item in the trial balance. Accumulated depreciation on the balance sheet serves an important role in capturing the current financial state of a business. It is a contra-asset account a negative asset account that offsets the balance in the asset account it is normally associated with. Accumulated depreciation is a contra asset account that summarizes the cumulative depreciation charges made on fixed assets. The balance represents either profit or loss on the sale of asset and should be debited or credited in this account. Accumulated depreciation is the cumulative depreciation of an asset that has been recorded. Fixed assets are recorded at original acquisition costs in the balance sheet and accumulated depreciation shown below the total fixed assets is the contra account revealing how much was depreciated. As a fixed asset is recognized in the balance sheet at the Net Book Value ie. 4 Two more terms that relate to long-term assets.

Accumulated depreciation is usually not listed separately on the balance sheet where long-term assets are shown at their carrying value net of accumulated depreciation.

Fixed assets like property plant and equipment are long-term assets. A contra account is needed to make a balancing entry on the balance sheet. Accumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use. In such a scenario the effect on the income statement will be the same as if no depreciation expense happened. Because accumulated depreciation is a contra asset it appears on a traditional balance sheet. Fixed assets like property plant and equipment are long-term assets.

When the asset is sold other otherwise disposed of you should remove the accumulated depreciation at the same time. Accumulated depreciation is nothing but the sum total of depreciation charged until a specified date. The balance sheet is a document that displays the details of a companys financial resources and obligations at any point in time. Accumulated depreciation is a contra asset account that summarizes the cumulative depreciation charges made on fixed assets. Accumulated depreciation is usually not listed separately on the balance sheet where long-term assets are shown at their carrying value net of accumulated depreciation. Accumulated depreciation is the total decrease in the value of an asset on the balance sheet of a business over time. Remove the asset from the balance sheet. This expense is tax-deductible so it reduces your business taxable income for the year. Fixed assets like property plant and equipment are long-term assets. The entry for the realization of periodic depreciation in ledger accounts is made by crediting accumulated depreciation against depreciation expense.

Since in every reporting period a part of a fixed asset is written off ie depreciated such accumulated depreciation has a credit balance. Accumulated depreciation is usually not listed separately on the balance sheet where long-term assets are shown at their carrying value net of accumulated depreciation. Remove the asset from the balance sheet. The balance sheet is a document that displays the details of a companys financial resources and obligations at any point in time. Accumulated depreciation till the date of sale on the respective asset and the sale proceeds from the disposal of the concerned asset are transferred to the credit side of this account. This expense is tax-deductible so it reduces your business taxable income for the year. Accumulated depreciation is subtracted from the assets cost to arrive at the net book value that appears on the face of the balance sheet. Accumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use. As a fixed asset is recognized in the balance sheet at the Net Book Value ie. Accumulated depreciation is the total decrease in the value of an asset on the balance sheet of a business over time.

There are 2 main methods of writing off an asset straight-line method and reducing balance. 4 Two more terms that relate to long-term assets. Fixed assets like property plant and equipment are long-term assets. Because accumulated depreciation is a contra asset it appears on a traditional balance sheet. Since in every reporting period a part of a fixed asset is written off ie depreciated such accumulated depreciation has a credit balance. It is calculated by the following formula. Updated May 07 2021. Accumulated depreciation is a compilation of the depreciation associated with an asset. The accumulated depreciation is shown as a credit item in the trial balance. Credit Machine Cost 2500.

Accumulated depreciation is a contra asset account that summarizes the cumulative depreciation charges made on fixed assets. For depreciation Accumulated depreciation opening balance Depreciation for the year - Accumulated depreciation of disposed asset In balance sheet it is showed as a substraction from the non-current asset to which it belongs. Cost less Accumulated Depreciation the machine will be removed from the accounts of ABC LTD in two parts. Some considerations when determining the value of an asset include depreciation purchase price book value and market. Accumulated depreciation on the balance sheet serves an important role in capturing the current financial state of a business. Accumulated depreciation is subtracted from the assets cost to arrive at the net book value that appears on the face of the balance sheet. Balance sheet depreciation is also known as accumulated depreciation and reduces the total value of the fixed assets. Accumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use. The balance represents either profit or loss on the sale of asset and should be debited or credited in this account. Since in every reporting period a part of a fixed asset is written off ie depreciated such accumulated depreciation has a credit balance.

Some considerations when determining the value of an asset include depreciation purchase price book value and market. This expense is tax-deductible so it reduces your business taxable income for the year. Fixed assets are recorded at original acquisition costs in the balance sheet and accumulated depreciation shown below the total fixed assets is the contra account revealing how much was depreciated. 4 Two more terms that relate to long-term assets. The entry for the realization of periodic depreciation in ledger accounts is made by crediting accumulated depreciation against depreciation expense. A Fixed asset has a value to a business and the value is written off over a fixed period of time. First the Machine Cost must be removed by crediting the ledger. Accumulated depreciation is subtracted from the assets cost to arrive at the net book value that appears on the face of the balance sheet. In such a scenario the effect on the income statement will be the same as if no depreciation expense happened. It is a contra-asset account a negative asset account that offsets the balance in the asset account it is normally associated with.